How Investors Actually Underwrite a Wholesale Deal

Most wholesalers look at one number:

ARV minus repairs minus contract price.

If there’s a spread, they assume it works.

That’s not underwriting.

That’s surface math.

Real investors underwrite differently. They don’t just calculate potential profit — they calculate risk, exposure, timing, and market direction.

If you want your wholesale deals to move consistently, you need to think like the buyer.

Here’s how investors actually underwrite a wholesale deal.

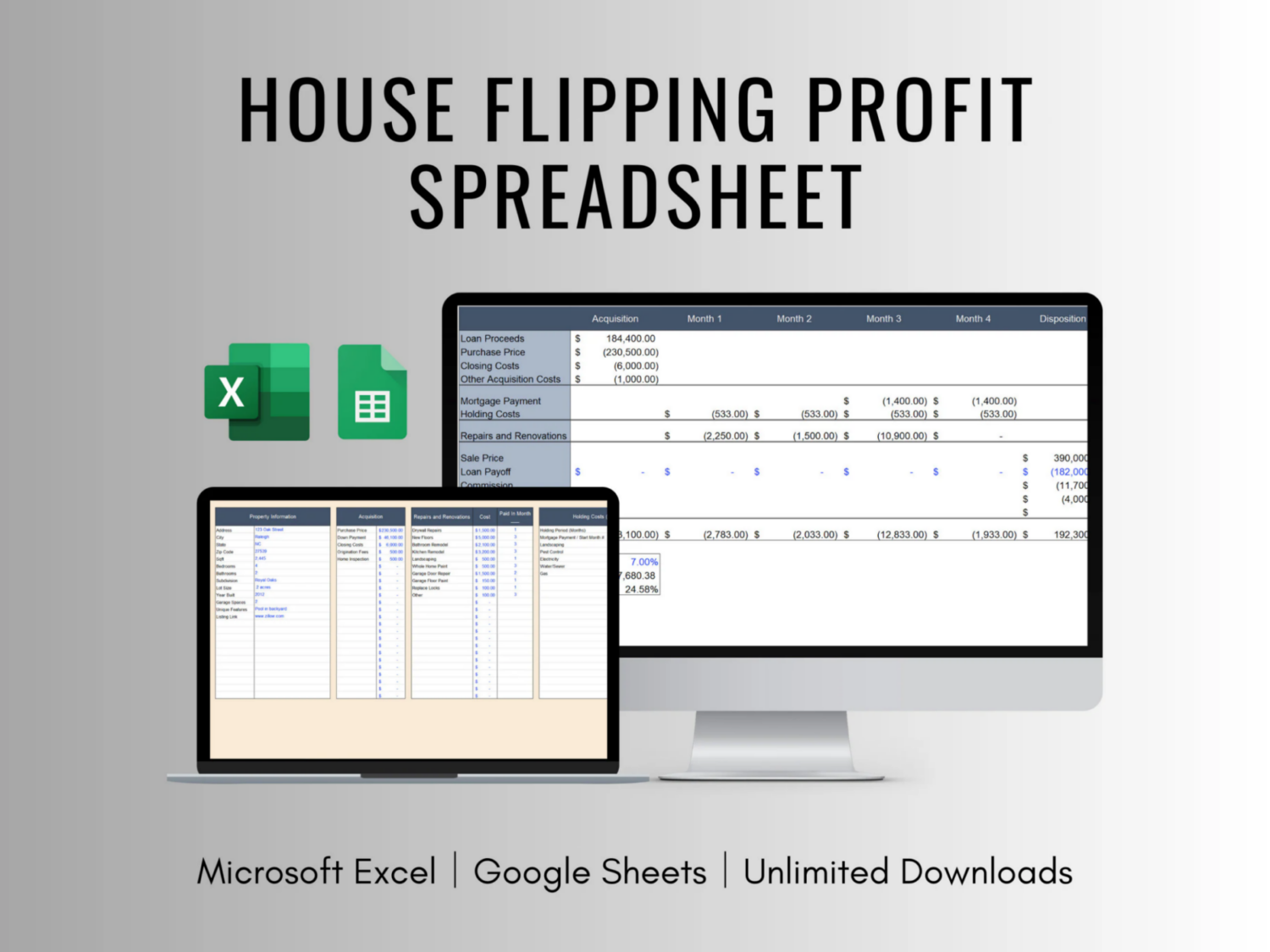

1. ARV — But Conservative

Investors don’t comp for the highest possible value.

They comp for the most defensible value.

We start with recent sold comps.

Then we look at:

-

Active listings

-

Days on market

-

Price reductions

-

Inventory levels

If similar houses are sitting at your projected ARV, that matters.

Because your buyer isn’t selling today.

They’re selling after rehab — in a future market.

If ARV requires perfect timing, it’s too optimistic.

(Internal link here to:

How to Know If Your Wholesale Deal Is Actually Good

2. Rehab — Padded, Not Optimistic

Most rehab numbers are light.

Investors assume:

-

10–20% overrun buffer

-

Material volatility

-

Contractor delays

-

Holding costs

If your rehab estimate is tight, the buyer will widen it.

Underwriting assumes margin compression — not expansion.

3. Margin Relative to Capital at Risk

This is where beginners miss it.

It’s not:

“How much profit is there?”

It’s:

“How much profit relative to how much capital is exposed?”

Example:

Risking $40k to make $25k = attractive.

Risking $75k to make $18k = unattractive.

Investors evaluate:

-

Cash tied up

-

Timeline

-

Opportunity cost

-

Liquidity risk

If capital is locked up too long for thin margin, the deal won’t move.

4. Market Direction

This is where active listings matter.

If comps from 3 months ago support your ARV, but current listings are sitting — the market may be softening.

Underwriting adjusts for:

-

DOM trends

-

Absorption rate

-

Price reductions

-

Inventory stacking

Investors price forward, not backward.

5. Structural Risk

Beyond numbers, buyers look at structure:

-

Clean title?

-

Clear exit strategy?

-

Clean access?

-

Seller timeline realistic?

-

Creative terms structured correctly?

If the structure feels messy, buyers hesitate.

Even good numbers won’t save poor structure.

6. Stress Testing the Deal

Strong deals survive stress testing.

Ask:

-

What if ARV is 10k lower?

-

What if rehab runs 15% over?

-

What if it takes 60 extra days to sell?

If small shifts kill the margin, buyers pass.

Investors underwrite assuming friction.

Why Most Wholesale Deals Don’t Move

It’s rarely one catastrophic mistake.

It’s usually:

-

Slightly stretched ARV

-

Slightly light rehab

-

Slightly heavy assignment

-

Slightly shifting market

All combined.

That stacking of risk is what kills deals.

Why Your Wholesale Deal Isn’t Selling

Before You Send It Out

Most wholesalers blast first and analyze later.

Professional investors analyze first.

If you want a real underwriting perspective before you send your deal to 5,000 buyers, send it here:

👉 Have Justin Review Your Deal

I primarily operate in Tennessee but review deals nationwide.

If it fits my buy box, I may take it down.

If it doesn’t, I’ll tell you why.

No hype. Just clarity.

Explore More Wholesale Deal Insights

Browse all articles in the Wholesale Deal Rescue section here:

👉 /category/wholesale-deal-rescue/