A Note Holder’s Guide to Foreclosure, Costs, and Better Options

Owning a mortgage note can feel like passive income—until the borrower stops paying.

At that point, many note holders in Tennessee realize they’re not just collecting payments anymore. They’re suddenly dealing with legal timelines, notices, attorneys, and real costs — which is why some ultimately choose to sell a mortgage note in Tennessee instead.

This guide walks through what really happens in Tennessee when a borrower defaults, how long it takes, what it costs, and when selling the note can be the smarter move.

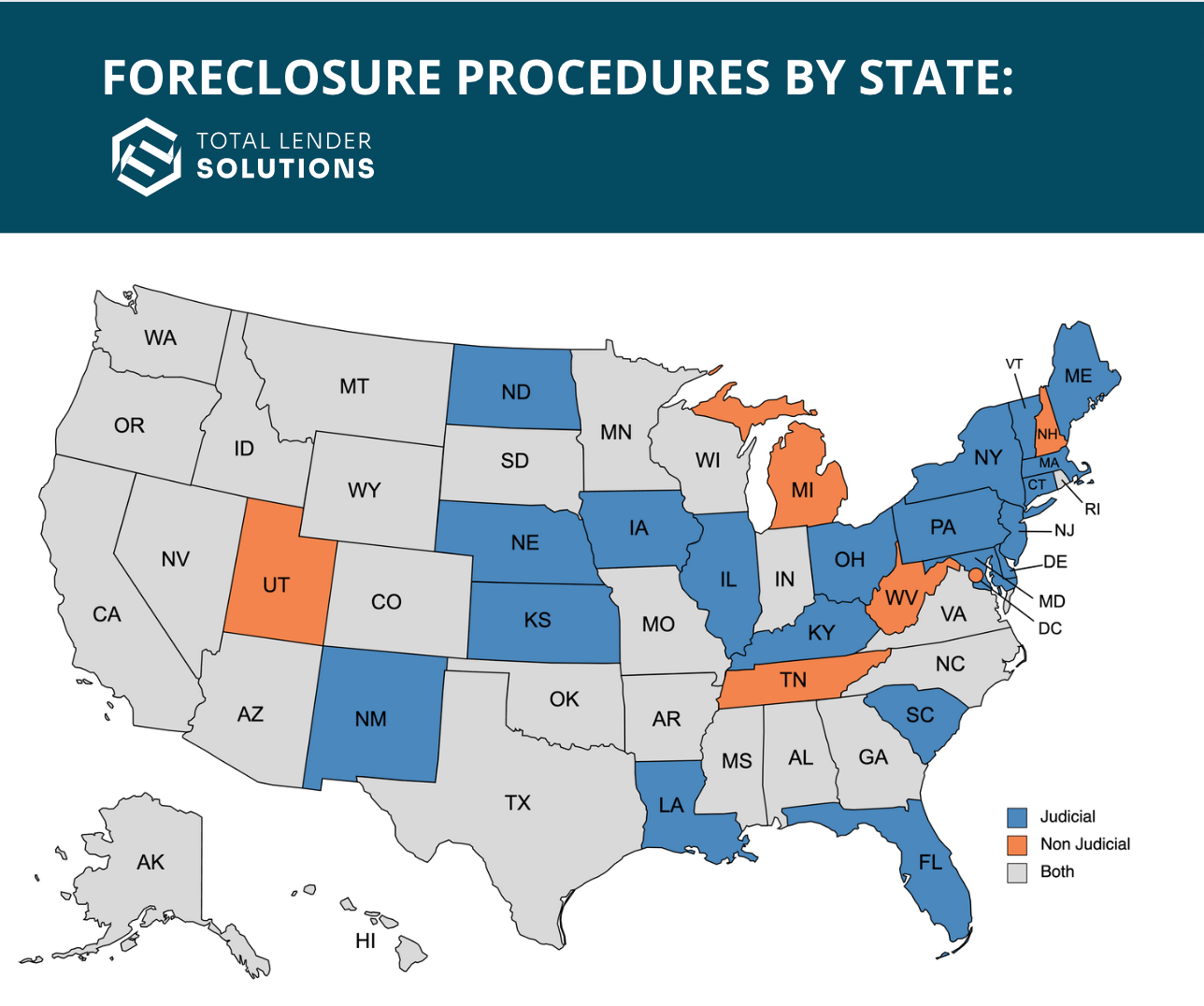

Tennessee Is a Non-Judicial Foreclosure State (But That Doesn’t Mean “Easy”)

Tennessee allows non-judicial foreclosure, which means lenders can foreclose without going through the court system—if the deed of trust allows it.

That sounds fast and simple. In reality, there are still strict steps that must be followed.

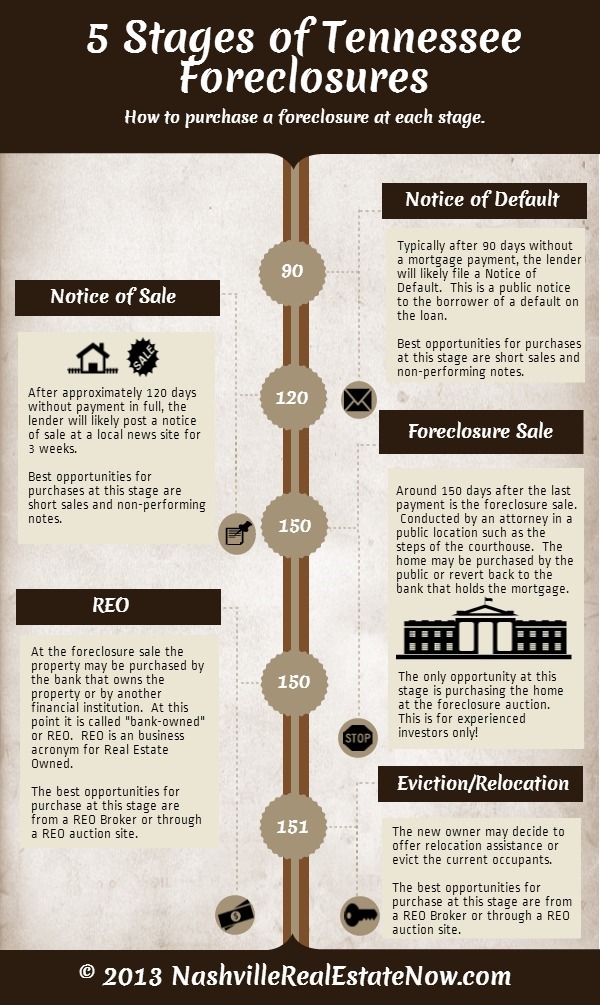

Typical Tennessee Foreclosure Timeline

-

Missed payments (usually 30–90 days delinquent)

-

Default notice sent to borrower

-

Acceleration notice (full balance demanded)

-

Newspaper publication (3 consecutive weeks)

-

Foreclosure sale (usually courthouse steps)

Best case: ~90 days

Common reality: 4–6 months (or longer if complications arise)

The Hidden Costs Most Note Holders Don’t Expect

Even without court involvement, foreclosure is not free.

Common Costs in Tennessee

-

Foreclosure attorney: $2,500–$4,000

-

Publication & trustee fees: $600–$1,200

-

Property preservation / securing: $500–$3,000

-

Taxes, insurance, utilities (while unpaid): variable

-

Repairs after vacancy: often $10,000+

And all of this happens while payments are not coming in.

One mistake many note holders make is assuming the property will be in good condition once they take it back. Unfortunately, deferred maintenance, vandalism, or abandonment are common.

Foreclosure Risk Isn’t Just Financial — It’s Emotional and Time-Consuming

Foreclosure isn’t just paperwork. It means:

-

Repeated follow-ups

-

Attorney coordination

-

Monitoring deadlines

-

Uncertainty about property condition

-

Stress over sunk costs

For part-time investors, retirees, or passive note holders, this can quickly become overwhelming.

When Selling the Note Makes Sense

-

The borrower is already behind

-

The margin of error is small

-

One foreclosure wipes out years of returns

-

You don’t want to manage property rehab or resale

-

You want to redeploy capital into something simpler

A note buyer assumes the risk, timeline, and management—so you don’t have to.

How We Approach Tennessee Notes Differently

At Rogers Investment Properties, we buy performing, re-performing, and non-performing notes in Tennessee.

We look at:

-

Remaining balance vs. property value

-

Borrower history

-

Property location and condition

-

Foreclosure risk and timeline

There’s no obligation, no pressure, and no “list it and wait” approach. Just a straight analysis and a clear offer.

If Your Borrower Has Stopped Paying — You Have Options

Foreclosure is one option.

Selling the note is another.

If you’re unsure which path makes sense for your situation, we’re happy to walk through it with you.

Reach out through our note submission form or contact us directly to discuss your Tennessee note—confidentially and without pressure.