ARV vs Reality: Why Comps Alone Don’t Make a Deal Work

If you’ve been wholesaling for any amount of time, you’ve heard this:

“ARV is $250K. The comps prove it.”

But here’s the problem.

Comps show you where the market was.

They do not tell you where it’s going.

And they definitely don’t guarantee what your buyer will actually sell for.

If your entire deal depends on one number pulled from past sales, you’re not underwriting.

You’re anchoring.

The ARV Illusion

Most wholesalers build deals like this:

Highest comp

– Rehab

– Profit

– Fee

= Contract price

That works in a rising market.

It fails in a shifting one.

Because ARV isn’t a fixed number.

It’s a moving target.

And if you haven’t read this yet, this explains how investors actually think through it:

How Investors Underwrite Wholesale Deals

Buyers don’t underwrite the best comp.

They underwrite the most probable exit.

Sold Comps vs Active Listings

Sold comps are historical.

Active listings are competitive.

If you have:

-

One sale at $250K

-

Two active listings at $245K sitting 60+ days

-

One price reduction to $239K

Your ARV isn’t $250K.

It’s under pressure.

This is exactly why some deals “look good” but collapse under scrutiny. We broke that down here:

When a Wholesale Deal Looks Good — But Isn’t

Because ARV confidence without velocity analysis is false confidence.

Velocity Is the Missing Variable

Velocity answers:

How fast are homes actually selling?

If DOM shifts from:

18 days → 35 days

35 days → 60 days

That changes everything.

Longer velocity means:

-

More holding costs

-

More financing exposure

-

More market risk

-

Greater chance of price compression

If you don’t factor time into pricing, you’re overstating value.

Comps Don’t Account for Market Direction

Comps don’t tell you:

-

If inventory is rising

-

If buyer demand is shrinking

-

If absorption rate is weakening

-

If price reductions are accelerating

That’s forward-looking risk.

And forward-looking risk is what investors price.

If you’re pricing based only on backward-looking comps, you’ll keep wondering:

“Why isn’t my wholesale deal selling?”

This article connects directly:

Why Your Wholesale Deal Isn’t Selling

It’s rarely about your buyer list.

It’s usually about compressed reality.

The Compression Effect

Let’s say ARV shows $250K.

In a neutral market, that might hold.

In a slowing market, investors may:

Compress ARV 5–10%.

Now you’re underwriting $225K–$237K instead.

That shift alone can erase:

-

Your assignment fee

-

The buyer’s margin

-

The deal entirely

This is why pricing discipline matters so much. If you missed it:

The 5 Pricing Mistakes New Wholesalers Make

Comps don’t protect you.

Margin does.

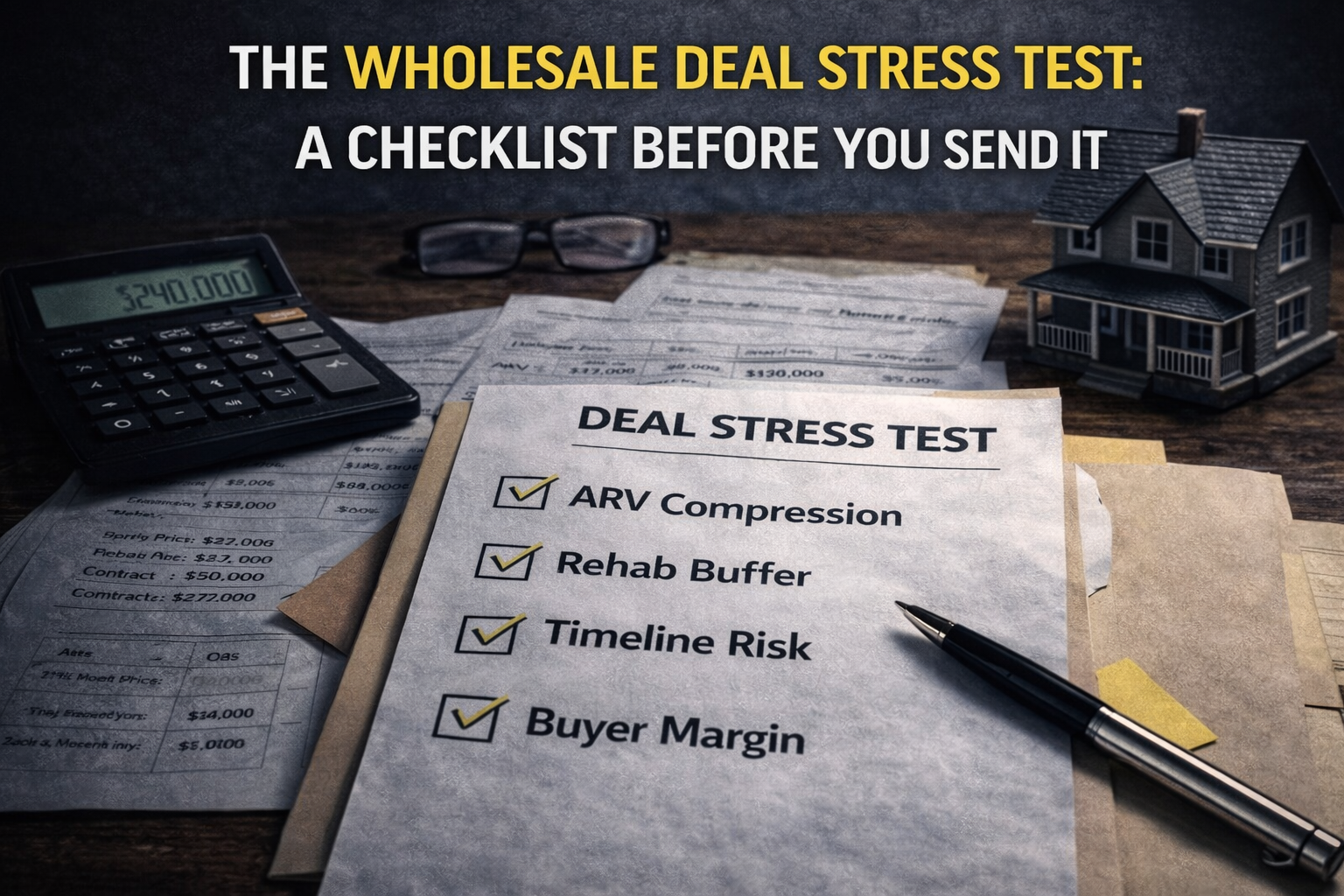

What Reality-Based ARV Looks Like

Serious investors evaluate ARV using:

-

Lowest reasonable comp (not highest)

-

Current active competition

-

DOM trend

-

Price reduction frequency

-

Absorption rate

-

Exit timeline

Then they stress-test:

-

5% ARV compression

-

10–15% rehab overrun

-

30–60 day sale delay

If it still works?

Now you have a real deal.

Why This Matters for Your Reputation

If you consistently send out deals priced off peak comps:

Buyers notice.

They start discounting your numbers before even reviewing them.

But when buyers know your ARVs are conservative?

They move faster.

Trust compounds.

If You’re Not Sure About Your ARV

If you’re sitting on a deal and questioning whether your ARV is real or optimistic, submit it for review here:

Wholesale Deal Review – RogersIP

We don’t save bad deals.

But we will pressure-test the numbers.

Explore More Wholesale Underwriting Breakdowns

For more tactical analysis on pricing, stress testing, and deal structure: